July 18, 2025 • 7 min read

Table of Content

Family caregiver income may be taxed, depending on who pays and what kind of payments they are. If you get money from Medicaid programs like CDPAP or IHSS, you may be able to get tax breaks. If a family member gives you cash, the IRS may see it as taxable income. Knowing how caregiver payments are reported can help you avoid tax surprises. Some caregivers may still have to pay taxes even if they don't make much money. This tutorial covers the rules to help you understand when caregiver income is taxable and what exemptions can apply.

Family caregivers may be paid for their work by several sources, depending on the situation. State laws say that family members can get paid for caring for someone through Medicaid programs like CDPAP in New York or IHSS in California. The Program of Comprehensive Assistance for Family Caregivers (PCAFC) gives stipends to family caregivers as well. Family caregivers may be able to get money back from long-term care insurance, but only if the policy allows it. The most common private compensation is when a loved one pays you directly from their wages or savings. The tax effects of each source are different, especially when it comes to how payments are reported.

Your classification also affects your taxes. If you are an independent contractor, you will get a 1099 form. You will be responsible for paying your taxes and reporting your income if you are an employee; your employer, whether a family member or an agency, may withhold taxes and give you a W-2 form. Families can make their caregiver arrangements without any formalities. Even though they often escape tax withholding, they need to be declared income in many circumstances. Knowing the differences between contractor, employee, and private family arrangements will help you better grasp what income is taxed and what you must disclose during tax season.

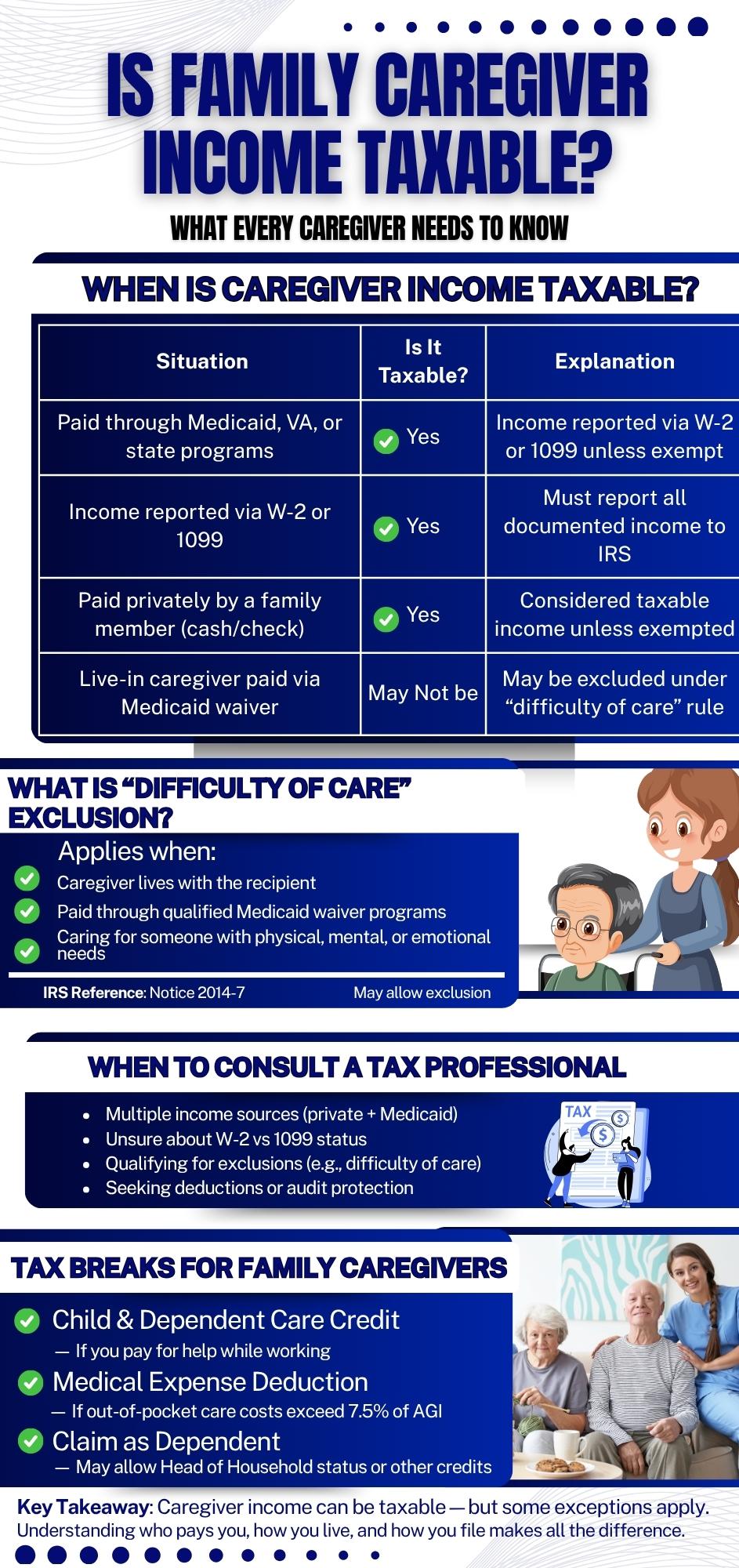

Situation | Is the Income Taxable? | Explanation |

Paid through Medicaid, VA, or government programs | Yes, typically taxable | Income is often reported to the IRS using W-2 or 1099 unless specific exemptions apply. |

Income is reported via 1099 or W-2 | Yes | If the income is officially documented, the IRS expects it to be reported and taxed. |

Caregiver does not live with care recipient | Yes | Living separately removes eligibility for specific exclusions like difficulty of care. |

Caregiver lives with care recipient and is paid under Medicaid | May not be taxable | IRS often excludes this income under the "difficulty of care" provision. |

IRS difficulty of care exclusion applies | May not be taxable | Designed to exclude income for care of an individual with disabilities when the caregiver lives in the same household. |

IRS Publication 525 tells you what kinds of income you must disclose and what you don't. This paper says that most payments given to family caregivers for services are taxable, unless there is a unique exception. IRS Notice 2014-7 makes a big provision that affects caregivers who work in the home. This notice says that some Medicaid waiver payments may be taken out of gross income if the caregiver lives with the person who needs care. We refer to these payments as difficulty of care payments.

The IRS calls it "difficulty of care" when you get paid for caring for people with physical, mental, or emotional problems that demand more attention. You might not have to report this income on your tax return if you meet specific qualifications, like living in the home and getting paid through a qualifying program. However, not all programs and caregiving arrangements meet these requirements, so thinking carefully about each is essential.

Caregivers may get more than one tax form, depending on how they are paid. If you work as an independent contractor, you usually get a 1099-NEC showing all of your profits. If you work for an agency or a private family, you will get a W-2 showing your pay and the taxes taken out of it. This is often the situation when you are a household employee. The IRS utilizes these forms to help you determine how to report your income.

If you get a 1099-NEC, you may also have to pay self-employment tax because you usually report your income on Schedule C with your Form 1040. If you get a W-2, your 1040 will disclose your wages. In all cases, you usually have to pay Social Security and Medicare taxes, unless you qualify for specified exclusions. If you get your income from Medicaid and it fits the requirements for difficulty of treatment, for example, you might not have to pay these taxes. Keep detailed records at all times to avoid problems when you file.

Family caregivers may be eligible for tax credits or deductions depending on their circumstances. Here are some important choices to consider:

Child and Dependent Care Credit: If you pay someone else to care for your loved one while you work or look for work, you may claim this credit. The person receiving care must be unable to care for themselves and live with you for at least half the year.

Medical Expense Deductions: If you pay for medical care or supplies out of pocket, and those costs exceed 7.5% of your adjusted gross income, you may deduct those expenses. This applies even if the person isn't your dependent, as long as you provide over half of their support.

Dependent Exemptions: While personal exemptions are no longer available, you may still claim the care recipient as a dependent. Doing so may open eligibility for other tax breaks like head of household filing status or additional credits.

If you're not sure if your caregiver payments are taxable, especially if you get money from more than one source, you should talk to a tax professional. It can be hard to figure out which amounts need to be reported and which don't when private family pay and government program revenue are added together. A tax expert can help you use the IRS's "difficulty of care" criteria to determine the proper worker classification and ensure your paperwork is sent in correctly. They can also help you find credits or deductions you might not have thought of. Getting expert assistance can help you avoid tax problems and audits if you pay for long-term care with stable income.

If you qualify under IRS Notice 2014-7 and live with the care recipient, your income from Medicaid caregiver programs could not be taxed. That income is typically taxed and needs to be disclosed if you don't fulfil the requirements.

VA caregiver payments are generally not taxable, particularly when made under the Program of Comprehensive Assistance for Family Caregivers. They are not required to be declared as income on your federal tax return since the IRS considers them non-taxable benefits.

Family caregivers are categorized as independent contractors and usually receive a 1099-NEC; if they are classed as employees, they often receive a W-2. Who pays them and the legal structure of the caregiver agreement determine the type of form.

According to IRS rules, payments to caregivers that meet the criteria for difficulty of care payments may not be included. To be eligible, the caregiver must live with the person they are caring for and be paid through specific Medicaid waiver programs outlined in IRS Notice 2014-7.

You must pay self-employment tax if you are an independent contractor and get a 1099-NEC. This includes both Medicare and Social Security. If you qualify for tax-exempt difficulty of care payments, you may not have to pay self-employment tax.

Your caregiver income may or may not be taxed, depending on who pays you, what kind of work you do, and whether you live with the person you care for. The IRS rules, like the complexity of care exemption, can only lessen or even eliminate your tax bill in certain situations. Filing incorrectly could lead to fines or lost credits. Because of this, knowing the laws before tax season is essential. GoInstaCare gives family caregivers trustworthy job options and valuable tools to help them deal with challenging financial problems. If you're not sure what to do, a skilled tax professional can help you record your income correctly and avoid costly mistakes.

Cities

Houston

Dallas

Austin

San Antonio

Miami

Chicago

Find Here

Companies