August 15, 2025 • 11 min read

Table of Content

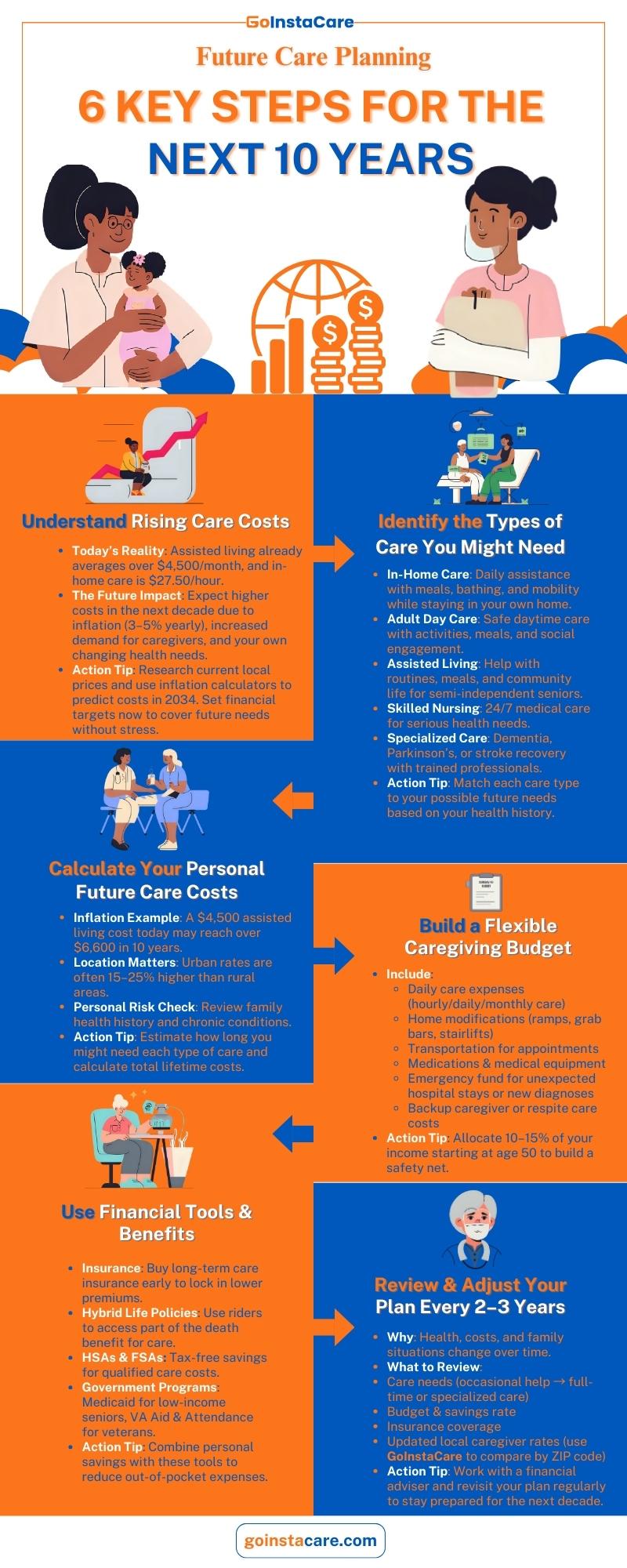

The first step in planning care for the next 10 years is to think about how costs increase. Care services already carry significant costs today, with assisted living averaging over $4,500 per month. Planning for the next decade means factoring in inflation, demand, and possible changes in your health and mobility. Over time, costs may rise because of inflation, higher demand, and possible health problems. It's a good idea to look at the current prices in your area and evaluate how much care you would require. This way, you may set a financial goal that will help you stay safe in case of an emergency and make sure you can get the help you need right away.

People in the U.S. are living longer, and that means more folks will need care as they age. Because of this, it’s important to start planning early. As the demand for caregivers and care facilities grows, prices often go up. If you wait too long, you can have less choices and more stress over money.

Most people need some care by their late 70s. If families don’t plan, they scramble to find affordable caregiver support during a stressful time. Planning early allows you to explore care choices and check your current spending, and estimate how much costs might increase.

What starts as a little help can turn into daily or full-time support. You can match your care needs with your insurance and savings goals. This helps you to stay comfortable.

In-home care: In-home caregivers help with everyday tasks like bathing, getting dressed and cooking meals. This kind of support allows you to stay in your own home more comfortably.

Adult day care: They offer a safe place during the day with meals, activities, and social time. It gives caregivers a break while helping seniors stay active and interact.

Assisted living: They provide meals, help with daily routines, and offer chances to socialize. It is great for those who need some support.

Skilled nursing: They offer 24/7 medical care and rehab from licensed caregivers. It is meant for people with serious or long-term health needs.

Specialized care (dementia, Parkinson’s, stroke recovery): They focus on complex health conditions with trained staff and therapies that support comfort.

Projected cost of $5,000 over 10 Years by the Inflation Rate.

Care Type | 2024 Cost | Estimated 2034 Cost |

In-home care (per hour) | $27.50 | $40.71 |

Assisted living (per month) | $4,500.00 | $6,661.10 |

Nursing home (per month) | $9,000.00 | $13,322.20 |

Year | 3% Inflation | 4% Inflation | 5% Inflation |

0 | $5,000.00 | $5,000.00 | $5,000.00 |

1 | $5,150.00 | $5,200.00 | $5,250.00 |

2 | $5,304.50 | $5,408.00 | $5,512.50 |

3 | $5,463.64 | $5,624.32 | $5,788.13 |

4 | $5,627.54 | $5,849.29 | $6,077.53 |

5 | $5,796.37 | $6,083.26 | $6,381.41 |

6 | $5,970.26 | $6,326.59 | $6,700.48 |

7 | $6,149.37 | $6,579.65 | $7,035.50 |

8 | $6,333.85 | $6,842.84 | $7,387.28 |

9 | $6,523.86 | $7,116.55 | $7,756.64 |

10 | $6,719.57 | $7,401.21 | $8,144.47 |

Take an honest look at your medical background. Conditions like diabetes, dementia, or heart disease, especially if they run in your family, can affect the kind of care you’ll need and how long you’ll need it. If you’re living with a chronic illness, it’s smart to expect small changes in your ability to manage daily tasks over time. Knowing your health risks helps you plan better for future care and costs.

Your location and lifestyle play a big role in shaping your care needs. If you live nearby hospitals or clinics, you are very much safe when you age. But if you’re in a rural or remote area, getting around could become harder, and you may need more support at home or in a care facility.

Having support from a spouse, adult children, or close friends can make a big difference. Consider paying trusted family members who help provide care, through available government or personal funds. Still, it is important to be realistic about how much families can support and help. Relying too much on family without a backup plan may lead to unexpected expenditures. Even if you stay independent for a long time, the final decade of life can bring big changes in your body.

Daily care costs: It is spent on things like home aides, assisted living, or nursing care that depends on how much support you need day to day.

Home modifications: This includes updates like ramps, grab bars, stairlifts, wider doorways, or safer bathrooms to make your home easier and safer to live in as you age. Together, these categories help you build a realistic, flexible budget to meet your care needs over time.

Transportation: You have to keep money aside for transportation during doctor visits, therapy, or social outings.

Medications and equipment: These present costs for prescriptions, mobility tools, medical equipment, and health trackers can help you stay healthy.

Emergency fund for unexpected needs: A backup plan for emergency hospital visits or new health issues that can pop up without warning.

Hiring backup help or respite care: It may cost extra funds to bring a temporary caregiver when your permanent caregiver is absent.

Once you reach age 50, it is a smart move to start setting aside 10–15% of your income for future care requirements. This gives you time to build a solid safety net before you need it. Even if you’re already 50, starting it now can still make a big difference, especially if you adjust your spending on things.

If you save $400 a month and your investments increase over time. In 10 years, you could have around $60,000. That money can help with assisted living costs or pay for several years of part-time home care. Starting earlier or saving more each month can grow that total even more.

If you qualify, a Health Savings Account (HSA) is a great way to save. You don’t pay taxes on the money you put in, and you don’t pay taxes when you use it for approved medical expenses, including some long-term care costs. That means your savings grow tax-free and can be spent tax-free, making it more cost-effective than regular savings. By using tax-friendly accounts and sticking to monthly contributions, you’ll be better prepared for whatever care you might need down the road.

Buying long-term care insurance is one of the simplest ways to plan. It can help cover the cost of nursing homes, assisted living, or care at home, so your savings don’t take a big hit. The earlier you buy, the lower your monthly premiums are likely to be.

Some life insurance plans offer long-term care riders, allowing you to use part of the benefit to cover care costs. These will enable you to use part of your policy to pay for care if you ever need it. If you don’t end up needing care, your loved ones still receive the life insurance payout. It’s a flexible option that protects both your future and your family.

Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs) offer tax benefits when saving for medical costs. HSAs are especially useful; they roll over year to year and can be used for long-term care in retirement. FSAs don’t carry over, but they’re still helpful for covering yearly care-related expenses.

If you qualify, programs like Medicaid and the VA Aid & Attendance benefit can help with care costs. VA Aid & Attendance supports veterans and their spouses with care at home or in a facility. Medicaid offers a wide range of services for people with lower incomes, including long-term care.

Care Type | Urban Average Cost | Rural Average Cost |

In-home care (per hour) | $30 | $25 |

Assisted living (per month) | $5,000 | $4,000 |

Nursing home (per month) | $9,500 | $8,000 |

If you’re trying to figure out how much care might cost in the future, online calculators can be a big help. Many tools let you compare prices for nursing homes, assisted living, and in-home care based on your city or county. You can even estimate how those costs might grow over the next 10 to 20 years with inflation. This makes it easier to adjust your budget.

GoInstaCare makes it even easier. You can search by zip code to find a caregiver near you and then check for hourly or monthly prices, and look for caregivers who match your care requirements and budget. Having clear, local information helps you make smarter choices.

Use GoInstaCare to explore caregiving options and costs in your ZIP code.

It is a good idea to review your caregiving plan and update it based on the situation for every 2 to 3 years. Your health and finances may change and your care needs might shift from occasional help to specialized support. Checking in regularly helps you spot these changes early so that you can adjust your insurance, savings goals, and care preferences before an emergency forces you to make rushed and often expensive decisions. Staying ahead keeps your plan realistic.

Working with a financial adviser can make these updates smoother. They can help you track inflation in your area and review how your investments are working. Advisers can also suggest updates to your insurance, savings rate, or investment strategy to keep your plan based on your situation. If your finances are complex, this kind of guidance can help you avoid coverage gaps and unnecessary tax issues.

GoInstaCare makes planning easier by showing you the latest caregiver prices in your area. You can check hourly, daily, or monthly prices and see how costs are changing over time. Checking your budget for every year helps you to plan for the future. You should be ready for anything that comes up in the next ten years of caring.

The costs of caregiving can be very different, but many families pay between $30,000 and $80,000 a year, depending on where they live, what sort of care they need, and how many hours they need it. These estimates may not include the full cost of full-time or specialized care.

The simplest way to do this is to find out what the current prices are in your area, factor in the level of care you expect to get, and use a 3–5% yearly inflation rate. This gives us a good idea of how much care will cost in the future.

Starting at age 50, try to save 10–15% of your income, which is about $300–$500 a month. Make changes based on where you live, your health, and inflation predictions so that you can comfortably pay for long-term care costs.

Medicare usually only covers short-term medical needs, not long-term care. Because Social Security only pays income and does not directly pay for care, most of the costs of caring for someone must be paid for using savings, insurance, or other forms of help.

If you can't pay for care, look into Medicaid, veterans' benefits, community programs, or services that charge based on how much you can afford. By planning and seeking financial counsel, you can get help at a fair price without giving up your quality of life.

Long-term care insurance, hybrid life insurance with care riders, Health Resources Accounts, and government programs like Medicaid or VA Aid & Attendance can help you pay for future caregiving costs without putting your money or resources at risk.

Family members can save money by providing care, but it's important to think about their long-term commitment, availability, and skill level. Some organizations even pay for family caregivers to help them with their financial and personal caregiving tasks.

The cost of caregiving differs from state to state through earnings, living costs, and service availability. Rural places may be affordable, but they may not have many speciality treatments. Urban areas usually cost more.

Yes, since care prices usually increase by 3 to 5% a year, account for inflation while creating your budget. Ignoring it can result in underfunding, which will make it more difficult to pay for the same kind of treatment later on.

Caregiving expenses can be deducted from taxes, including medical treatment, home improvements, medical equipment, and other in-home services. The IRS program sets the rules, and so it is important to keep good records and get professional tax advice.

It’s not ideal to wait until the last minute to make care decisions. Planning helps you stay in control and reduces stress. But when you plan, you remain in control of your future. Even small savings can help you afford the care you need for your comfort. It is important to check updates based on your health.

Explore Instant Quality Care for your Loved Ones to find trusted caregivers. With the support, you can face the future with confidence knowing your loved ones will be cared for with comfort and dignity.

Cities

Houston

Dallas

Austin

San Antonio

Miami

Chicago

Find Here

Companies