September 03, 2025 • 6 min read

Table of Content

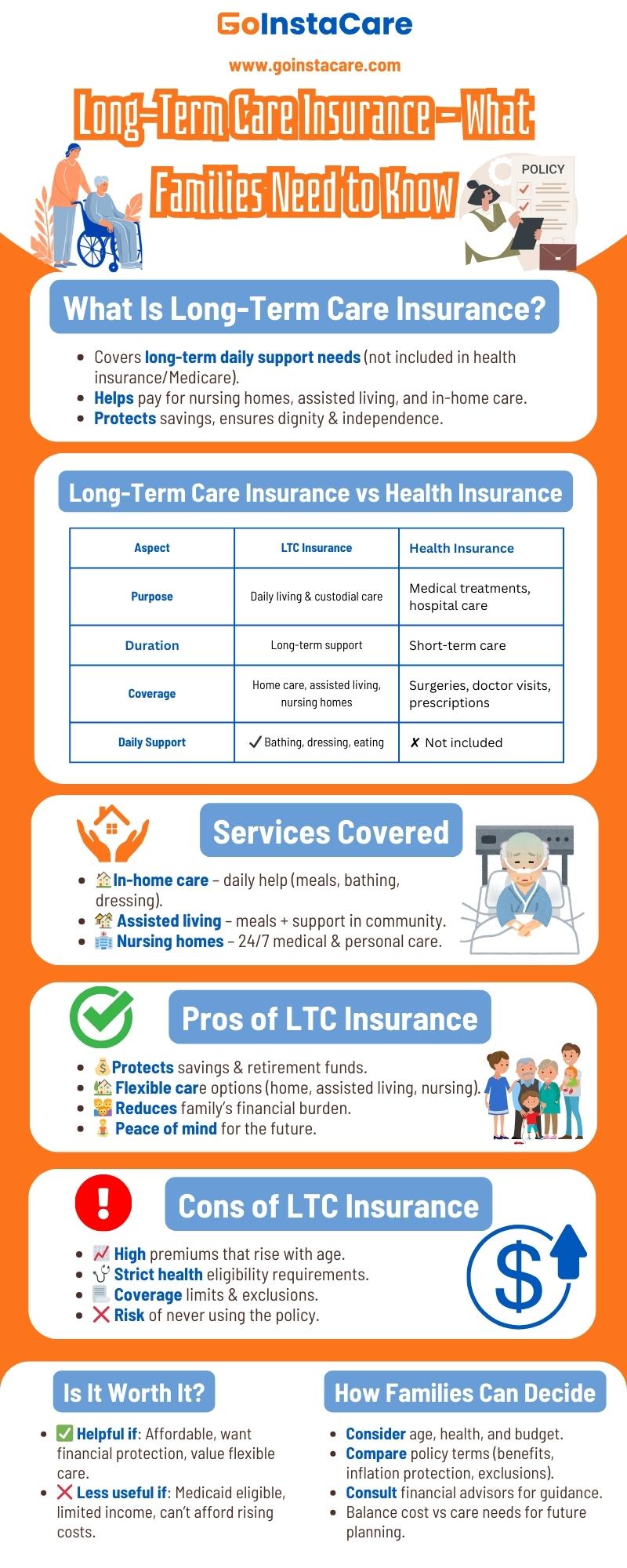

Long-term care insurance helps pay for the high costs of services like assisted living, nursing homes, or in-home care that regular health insurance and Medicare often don't cover. Families usually have pros and cons of long-term care insurance before choosing. To plan for becoming older or having health problems, you need to know how it works and its pros and cons. Families can help them to make wise choices that have equal balance to their need for care and financial stability.

Long-term care insurance helps seniors to pay for the costs of care for those who help with daily tasks because they are becoming older. Long-term care insurance pays for long-term care services that regular health plans usually don't cover. This differs from regular health insurance, which primarily pays for short-term medical needs like hospital stays, doctor visits, or prescriptions.

Its primary goals are to make it easier for families to make ends meet, protect their savings, and ensure that people can get good care in nursing homes, assisted living facilities, and even their own homes. This insurance provides a safety net that lets people keep their independence and dignity while getting the care they need as healthcare prices rise. Families often see it as a way to make sure their loved ones get continuous, reliable support without running out of money and are ready for problems that may come up in the future.

Aspect | Long-Term Care Insurance | Health Insurance |

Purpose | Covers extended personal and custodial care needs | Covers medical treatments, doctor visits, and hospital care |

Duration | Focuses on long-term, ongoing support | Focuses on short-term or acute care |

Coverage | Nursing homes, assisted living, home care | Surgeries, hospital stays, prescriptions |

Daily Living Support | Yes, includes help with bathing, dressing, eating | No, does not cover personal care needs |

In-home care for daily assistance such as bathing, dressing, and meal preparation.

Assisted living facilities provide meals and support in a community setting.

Nursing home care for seniors for needing 24/7 medical and personal support.

Long-term care services are expensive and insurance helps pay for them that protects savings and retirement funds. It prevents families from using their money when they need long-term care.

Policies often allow people to select where they get care like at home, in assisted living or in a nursing home. This gives families control over the kind of assistance they require.

Family members may have to pay a lot of money without insurance. Insurance will pay for seniors so that families don't have to spend a lot of money and reduce their burden.

Knowing care needs will be covered provides reassurance. It allows individuals and families to plan confidently, avoiding uncertainty and ensuring dignity during ageing or health challenges.

The cost increases significantly as seniors get older. This makes policies less affordable for those who wait too long to apply, creating a financial strain on retirement planning.

Applicants must meet health requirements during the application process. Pre-existing conditions or chronic illnesses may lead to denial, making it difficult for some people to qualify for coverage.

Policies may exclude certain conditions, set daily or lifetime benefit caps, or restrict specific services. These limitations can leave policyholders with unexpected out-of-pocket expenses during extended care.

Some seniors may pay for years but never need long-term care services. This risk makes families question whether the investment in insurance is worth the potential outcome.

Long-term care insurance can be helpful but it depends on the person's situation. Having a policy ensures these groups may get high-quality services without spending more money in their retirement accounts or putting pressure from their family's finances.

But you might not always need long-term care insurance. For example, people with limited incomes or assets may get Medicaid that pays for long-term care services. The coverage may also become too expensive for folks who can't pay the rising costs.

You should also consider other options. Medicaid can help low-income people to pay for their medical care but they can also choose to pay for their own care with their own money. They give families more flexibility even if they never need long-term care.

Families should consider their age, health, and money before choosing long-term care insurance. People who are young usually pay less for insurance but people who are sick for a long time have to pay more. If an insurance policy is affordable and worth the money, you need to look at your income and your long-term financial goals.

It's also quite important to carefully compare the terms of the policy. Different plans offer different levels of coverage, benefit lengths, and protection against inflation. Families ensure exactly what is covered and what might cost them.

The choice might be easier if you talk to financial advisers and other professionals who care. Experts may look at each person's situation, find hidden costs, and discuss various options. Families may avoid problems and choose a plan that equally balances price and care needed with the guidance.

The main benefit of long-term care insurance is that it protects your money. It helps people and their families relax by preserving their savings, helping them pay for pricey caregiving services, and ensuring they have access to good care options.

Some of the problems with long-term care insurance are that it doesn't cover some things, has rigorous qualifying rules, and costs a lot. People worry about whether the investment is worth it in the long run and whether they can afford it because many people pay for years without getting the benefits.

Long-term care insurance premiums typically range from $2,000 to $4,000 yearly, contingent on age, health, and coverage choices. While older people pay far more for comparable benefits, younger applicants usually pay cheaper rates.

Long-term care insurance gives you more choices and better treatment than Medicaid or Medicare. Medicare only covers short-term requirements and Medicaid has mandatory income limits so insurance is more flexible and provides long-term financial stability.

People between the ages of 50 and 60 should think about getting long-term care insurance. Families can get coverage before the risk of chronic conditions increases, premiums go down, and achieving health requirements is easier.

There are pros and cons in long-term care insurance. Even though it gives flexibility and financial stability. To find you need to think about your age, health, and money. Before making a choice families should think about the specifics of the program and look at other choices like Medicaid or hybrid insurance. The major goal is to ensure that treatment succeeds and people can rest without worrying about money. GoInstaCare gives families reliable choices that are specific to their requirements to make sure they get help from qualified caregivers.

Cities

Houston

Dallas

Austin

San Antonio

Miami

Chicago

Find Here

Companies