July 17, 2025 • 8 min read

Table of Content

Medicare usually doesn't cover long-term caregivers who help with daily tasks like getting dressed, bathing, and making meals. It generally pays for short-term medical care that a doctor orders, including skilled nursing or physical therapy at home. Medicare usually doesn't pay caregivers who aren't trained in medicine and only help with personal care. This often surprises families who expect more help. Some Medicare Advantage plans may offer limited benefits for caregivers, though. Families can make better plans when they know what is and is not omitted. Most people must pay for full-time care or help at home through Medicaid, VA programs, or private insurance.

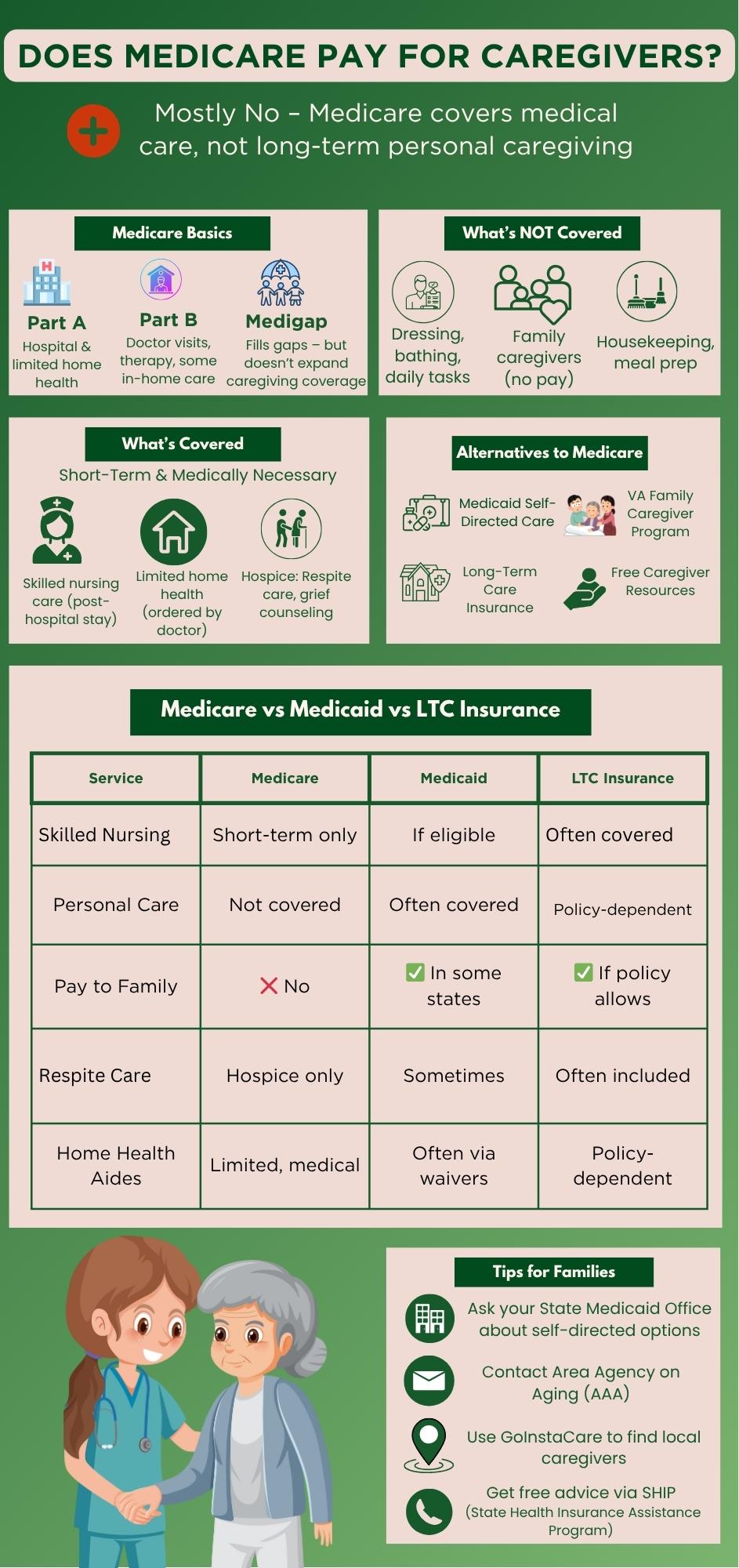

The first step to understanding how Medicare works is learning its parts. Part A of Original Medicare pays for hospital stays, and Part B pays for outpatient services like doctor visits and some home health care. Part C, or Medicare Advantage, is a commercial plan combining Parts A and B, often giving you more coverage.

Some Advantage plans might help with personal care or short-term in-home help, but the amount of help varies by provider and location. Medicare Supplement, sometimes called Medigap, helps pay for things that Original Medicare doesn't cover, but doesn't boost caregiver benefits.

Medicare's principal job is to pay for medical care. It stresses professional services, including physical therapy, nursing care, and injections administered by trained professionals. This differentiates it from private long-term care insurance or Medicaid, which might pay for daily care tasks. Under Medicare, a "caregiver" often helps a friend or family member without compensation. Medicare does not see these unpaid caregivers as billable providers. Instead, it only covers care from qualified medical experts when a doctor says it's necessary for a short time.

Medicare provides limited caregiving assistance, mainly related to medical requirements or end-of-life care. What each section might cover is as follows:

Short-term skilled nursing care in a facility after a qualifying hospital stay

Hospice care that includes caregiver support, like grief counseling and limited respite car

Home health care, but only if medically necessary and ordered by a doctor

Part-time skilled nursing care at home, such as wound care or injections

Physical, occupational, or speech therapy as part of a care plan

Medical social services like counseling and care coordination

Some plans cover non-medical in-home services, like help with bathing or dressing.

Transportation to medical appointments or pharmacies

Limited homemaker support, such as light housekeeping or meal delivery

These services frequently have stringent eligibility requirements and must be linked to a doctor-approved plan. Typically, coverage is temporary and not intended for continuous, day-to-day assistance with caregiving.

Medicare does not pay for long-term personal care services like dressing, feeding, and bathing if they are the only help you need. It won't pay for live-in caregivers or home care that lasts all day and all night either. Medicare does not cover meal preparation, cleaning, or laundry unless they are part of a Medicare Advantage plan.

Medicare does not pay family members who care for someone else, even if they help them daily. Because of these rules, many families must pay for things independently or get help from Medicaid, VA benefits, or private insurance. By knowing these limits, families can better plan for long-term care requirements beyond Medicare's medical focus and avoid surprises.

These services are available to families who need help with money or practical matters when Medicare won't pay for caregiving costs:

Medicaid (self-directed care programs): Some states let people hire family members, including spouses, as paid caregivers through waivers or home-based care options.

VA Caregiver Support Program: Offers monthly stipends, respite care, and training for family members caring for veterans with service-related disabilities.

Long-term care insurance: Private plans that may cover home or personal care services, including payments to family caregivers if the policy allows.

State-funded family caregiver programs: Some states offer cash assistance, respite care, or caregiver training through local health departments or aging networks.

Area Agency on Aging services: These agencies connect caregivers with local help, such as respite services, support groups, training, and care planning, not direct pay, but valuable resources.

Medicare will only pay for in-home help if it meets strict medical standards. If you stay in the hospital for three days or more, Medicare Part A may pay for skilled nursing or treatment at home through its home health benefit. Part B may also cover services that a doctor orders and says are medically necessary. The care must be offered by certified professionals part-time instead of full-time. This includes nursing, speech therapy, and physical therapy. Help with personal care may be covered, but only if it is related to medical care. Long-term help at home or daily care is not included.

Medicare does not pay family members directly to care for you, even if they help you daily. Traditional Medicare only pays for medically necessary services ordered by a doctor and provided by licensed personnel. Some Medicare Advantage plans might offer limited benefits through experimental models that include caregiver support or training, but don't pay directly.

These options aren't always available, and they depend on the plan. Families that require long-term care insurance, Medicaid self-directed programs, or VA help for caregivers should consider these possibilities. These sites make it easier for family caregivers to get money by showing how to get help from the state or federal government based on who is eligible, what kind of care is needed, and what kind of help is available.

Medicare's hospice coverage includes help for family caregivers caring for someone at the end of their life. It offers practical and emotional support through a hospice staff that teaches, counsels, and guides caregivers. Family members can obtain grief and loss therapy for up to a year after the patient dies. Medicare also offers a 5-day respite care benefit, which lets the caregiver take a short break while the patient stays in a facility that Medicare has approved. Even though hospice doesn't pay family caregivers directly, it helps them deal with the burden of caregiving and other responsibilities by providing comfort, information, and emotional support.

By comparing Medicare, Medicaid, and commercial long-term care insurance, families can better understand where to get help with caregiving. Medicaid covers greater long-term care, like paying family caregivers in some places, while Medicare mainly covers short-term medical care. Private long-term care (LTC) insurance can fill in gaps only if the policy allows it. Here's a little example:

Service Type | Medicare | Medicaid | LTC Insurance |

Skilled Nursing | Short-term only | Covered with eligibility | Usually covered |

Personal care | Not covered | Often covered (varies by state) | Covered if included in policy |

Pay to Family Caregiver | Not covered | Allowed in some programs | Possible if policy permits |

Respite Care | Hospice only | Sometimes covered | Often included |

Home Health Aides | Short-term with medical need | Covered under HCBS waivers | Covered if in policy |

If Medicare doesn't cover a family's care needs, they can combine it with Medicaid for more complete coverage. Dual eligible people may get both benefits, allowing them to receive long-term care benefits that Medicare alone can't give them.

Community resources like nonprofit caregiving networks or local Area Agencies on Aging (AAA) can help with transportation, meals, and short-term care. GoInstaCare is a dependable way to find competitively priced in-home caregivers matching your family's needs. Their service can help you when needed and lower your stress. Contact your state's SHIP (State Health Insurance Assistance Program) for free help with benefits, coverage options, and what to do next.

Medicare only pays for in-home caregivers when a doctor says they are needed for medical care. It doesn't pay for non-medical help like cooking, dressing, or bathing unless it's part of a limited Medicare Advantage plan.

No, Medicare won't pay you to take care of your spouse or parent. Only short-term medical care from licensed professionals is covered. Neither normal Medicare nor most Advantage plans pay family caregivers.

Medicare does pay for respite care, but only if the hospice benefit covers it. It offers family caregivers a vacation of up to five days in a Medicare-approved facility. Medicare does not cover hospice-related respite care.

Medicare doesn't pay for everyday care, but it does pay for short-term medical treatment. In some places, Medicaid helps people long-term, even paying family caregivers. Medicare has stricter rules on covering non-medical care and is based on age or disability. Medicaid, on the other hand, is based on income.

Some Medicare Advantage plans may pay for non-medical care services, although coverage is limited and varies by provider. Traditional Medicare doesn't cover help with ordinary tasks like getting dressed or making meals unless medically necessary.

Medicare generally pays for short-term skilled care that is needed for medical reasons and gives little help to caregivers. Families must take care of these things independently because it doesn't cover daily or long-term non-medical care. Families often use Medicaid, VA benefits, or private support services to fill these gaps. GoInstaCare fills this gap by connecting families with trustworthy, flexible caregiver options. GoInstaCare makes it easy to obtain reliable, personalized help at home, whether you need help for a short time or a long time.

Cities

Houston

Dallas

Austin

San Antonio

Miami

Chicago

Find Here

Companies